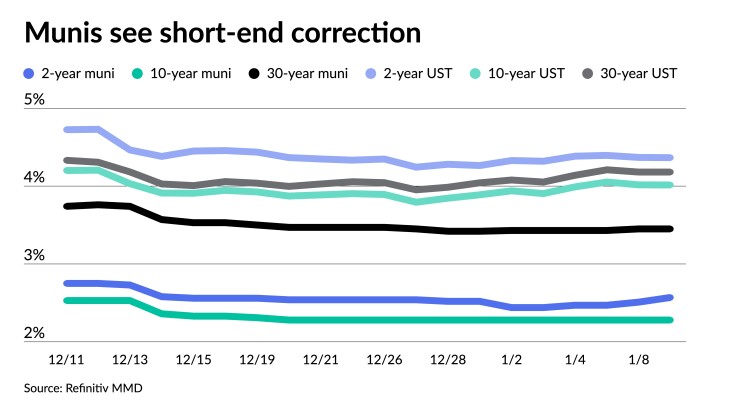

Municipals saw a short-end correction Tuesday, with the one-year being hit the hardest, amid two large deals in the primary market. U.S. Treasuries were little changed and equities ended down.

Triple-A yields rose six to 11 basis points on the short end, as more investors put pressure there amid what

The two-year muni-to-Treasury ratio Tuesday rose slightly as a result at 59%, the three-year at 59%, the five-year at 57%, the 10-year at 57% and the 30-year at 82%, according to Refinitiv Municipal Market Data’s 3 p.m. EST read. ICE Data Services had the two-year at 60%, the three-year at 59%, the five-year at 57%, the 10-year at 58% and the 30-year at 82% at 4 p.m.

While munis had rallied around 100 basis points since Nov. 1, last week’s reversal, which saw muni yields rise seven to eight basis points across the curve, gave back less than 10% of that, said Matt Fabian, a partner at Municipal Market Analytics.

Even more was given back Tuesday, at least on the short end of the curve, as the one-year was cut up to 11 basis points, depending on the scale, while there was weakness in others spots as well.

The offered curve is “still deeply overbought” at all maturities outside of one year, which is “a signal for issuers and sellers to become aggressive,” Fabian said.

“This also comports with a market facing a price discovery test amid a more normal calendar,” he said.

Both new-money and refunding issuance are apt to surge in this quarter “as borrowers catch up on opportunities delayed or unavailable last year,” according to Fabian. Bond Buyer 30-day visible supply sits at $13.47 billion.

Additionally, Fabian said, if inflows into muni mutual funds do not turn “steadily positive” soon, “it is also unclear how much further yields and ratios can or would fall with only [separately managed accounts and exchange-traded fund] buyers to drive them.”

This lack of inflows not only concerns performance concern but “to the extent it deprives the near-record current number of financings with technical defaults … of rescue capital, payment defaults are likely to rise faster than expected,” he said.

On the upside, the month of January tends to be a positive performance month, said AllianceBernstein strategists in a weekly report.

Over the past 15 years, munis have returned an average of 0.93%, according to Bloomberg. Munis are currently returning negative 0.22%.

While munis “have gotten out of the gate a bit sluggish … the technical environment does remain supportive” due to a lack of new-issue supply and sizable coupon payments, they noted.

This week’s $9.1 billion new-issue calendar should be easily absorbed by the market, AllianceBernstein strategists said.

The demand, they noted, “will be driven by relative value, not necessarily available cash.”

In the primary market Tuesday, RBC Capital Markets priced for Main Street Natural Gas (Aa1///) $836.645 million of gas supply revenue bonds, Series 2024A, with 5s of 3/2025 at 3.95%, 5s of 3/2029 at 3.82%, 5s of 9/2029 at 3.82% and 5s of 9/2031 at 3.95%, callable 6/1/2031.

Goldman Sachs priced for the Southeast Alabama Gas Supply District (Aa3///) $758.280 million of Project No. 1 gas supply revenue refunding bonds, Series 2024A, with 5s of 4/2025 at 3.94%, 5s of 2029 at 4.02% and 5s of 2032 at 4.08%, make whole call.

Loop Capital Markets priced for the Community College District No. 508, Illinois, (/AA/A+/) $186.560 million of BAM-insured dedicated revenues unlimited tax GO refunding bonds, Series 2024, with 5s of 12/2027 at 2.92%, 5s of 2029 at 2.92%, 5s of 2034 at 3.10%, 5s of 2039 at 3.64% and 5s of 2043 at 3.91%, callable 12/1/2033.

Stifel Nicolaus & Co. priced for the Agua Fria Union High School District No. 216, Arizona, (Aa1///) $141.55 million of GOs, with 5s of 7/2024 at 2.84%, 5s of 2027 at 2.46%, 5s of 2034 at 2.43%, 5s of 2039 at 3.00% and 5s of 2043 at 3.34%, callable 7/1/2033.

In the competitive market, the Stillwater Independent School District No. 834, Minnesota, (Aa1///) sold $161.830 million of GO school building, facilities maintenance and refunding bonds, Series 2024A, to J.P. Morgan, with 5s of 2/2025 at 2.91%, 5s of 2029 at 2.35%, 5s of 2034 at 2.41%, 5s of 2039 at 2.97% and 4s of 2044 at 3.73%, callable 2/1/2032.

Secondary market

Washington 5s of 2025 at 2.90% versus 2.71% Monday and 2.70% original Wednesday. Georgia 5s of 2025 at 2.77% versus 2.57% Wednesday. NYC 5s of 2026 at 2.60%.

Maryland 5s of 2028 at 2.37%. NYC 5s of 2028 at 2.42%. California 5s of 2029 at 2.31%.

Connecticut 5s of 2034 at 2.41%. Wisconsin 5s of 2035 at 2.38% versus 2.37% Monday. University of California 5s of 2035 at 2.17%-2.18%.

NYC TFA 5s of 2043 at 3.30%-3.28%.

AAA scales

Refinitiv MMD’s scale saw cuts three years and in: The one-year was at 2.83% (+10) and 2.57% (+6) in two years. The five-year was at 2.25% (unch), the 10-year at 2.28% (unch) and the 30-year at 3.45% (+2) at 3 p.m.

The ICE AAA yield curve was cut 10 basis points at one-year: 2.83% (+10) in 2025 and 2.60% (+3) in 2026. The five-year was at 2.30% (+2), the 10-year was at 2.29% (+1) and the 30-year was at 3.42% (unch) at 4 p.m.

The S&P Global Market Intelligence municipal curve saw large cuts on the short end of the curve: The one-year was at 2.81% (+11) in 2025 and 2.65% (+8) in 2026. The five-year was at 2.29% (unch), the 10-year was at 2.32% (unch) and the 30-year yield was at 3.41% (unch), according to a 3 p.m. read.

Bloomberg BVAL was cut up to six basis points on the front end: 2.74% (+6) in 2025 and 2.60% (+5) in 2026. The five-year at 2.28% (+2), the 10-year at 2.33% (+1) and the 30-year at 3.43% (+1) at 4 p.m.

Treasuries were little changed.

The two-year UST was yielding 4.361% (-1), the three-year was at 4.124% (-1), the five-year at 3.969% (flat), the 10-year at 4.012% (flat), the 20-year at 4.320% (flat) and the 30-year Treasury was yielding 4.180% (flat) near the close.

Primary to come

Jefferson County, Alabama, (Baa1/BBB+/BBB/) is set to price Wednesday

Massachusetts (Aa1/AA+/AA+/) is set to price Thursday

The Conroe Independent School District, Texas, (Aaa/AAA//) is set to price Wednesday $568.105 million of PSF-insured unlimited tax school building bonds, Series 2024, serials 2025-2049. Raymond James & Associates.

The Minnesota Agricultural and Economic Development Board (A2/A//) is set to price Wednesday $500 million of HealthPartners Obligated Group healthcare facilities revenue bonds, Series 2024. Piper Sandler.

The Lewisville Independent School District, Texas, is set to price Thursday $462.655 million of unlimited tax school building bonds, Series 2024. Piper Sandler.

New Braunfels, Texas, (Aa1///) is set to price Thursday $148.970 million of utility system revenue and refunding bonds, Series 2024, serials 2024-2055. HilltopSecurities.

Competitive

The Florida Board of Education (Aaa/AAA/AAA/) is set to sell $234.010 million of PPulic Education Capital Outlay refunding bonds, 2024 Series A, at 11 a.m. Wednesday.

Dallas is set to sell $223.620 million of combination tax and revenue certificates of obligation, Series 2024A, at 11 a.m. Thursday.