Municipals rallied hard Thursday, playing catch up to the moves in U.S. Treasuries, which extended their gains for a second session following the Federal Open Market Committee’s clear communication of future rate cuts in 2024. Equities continued their rally.

Triple-A yields fell 13 to 17 basis points, depending on the curve, but the gains were not near the two-day UST rally. UST yields fell another six to 16 basis points Thursday after falling upward of a quarter point Wednesday, pushing the 10-year UST below 4% for the first time since July 31.

Secondary muni trading showed clear strength across the yield curve, with bellwether names trading up significantly from recent prints and original pricing levels. New-issues in the primary benefited from the day’s moves with issuers from Illinois repricing to lower yields.

Ratios fell slightly on the day’s moves. The two-year muni-to-Treasury ratio Thursday was at 59%, the three-year at 59%, the five-year at 60%, the 10-year at 60% and the 30-year at 88%, according to Refinitiv Municipal Market Data’s 3 p.m., ET, read. ICE Data Services had the two-year at 58%, the three-year at 58%, the five-year at 57%, the 10-year at 59% and the 30-year at 85% at 4 p.m.

In the primary market Thursday, RBC Capital Markets priced and repriced for the Illinois State Toll Highway Authority (Aa3/AA-/AA-/) $889.275 million of toll highway senior revenue refunding bonds, 2024 Series A, with yields bumped up to 22 basis points: 5s of 1/2028 at 2.55% (-15), 5s of 2033 at 2.69% (-15), 5s of 2038 at 3.34% (-18) and 5s of 2039 at 3.40% (-22), callable 7/1/2034.

Jefferies priced for Chicago (//A/A/) $383.855 million of AMT Chicago Midway Airport senior lien airport revenue refunding bonds, Series 2023C, with 5s of 1/2025 at 3.64%, 5s of 2028 at 3.44%, 5s of 2033 at 3.52%, 5s of 2038 at 3.86% and 5s of 2041 at 4.05%, callable 1/1/2034.

In the competitive market, the New York State Urban Development Corp. (Aa1//AA+/) sold $334.625 million of state personal income tax revenue bonds, Series 2023B, Bidding Group 1, to Wells Fargo Bank, with 5s of 3/2025 at 2.68%, 5s of 2028 at 2.40%, 5s of 2033 at 2.45%, 5s of 2038 at 3.06% and 5s of 2042 at 3.39%, callable 9/15/2033.

The UDC also sold $251.180 million of climate bond-certified state personal income tax revenue bonds, Series 2023A, Bidding Group 2, to Jefferies, with 5s of 3/2034 at 2.50%, 5s of 2038 at 3.05%, 5s of 2043 at 3.40%, 5s of 2048 at 3.68% and 4s of 2053 at 4.12%, callable 9/15/2033.

The corporation also sold $246.955 million of climate bond-certified state personal income tax revenue bonds, Series 2023A, Bidding Group 3, to Truist Securities. Pricing details were not available at 4 p.m. Thursday.

Secondary trading

Maryland 5s of 2024 at 2.78% versus 2.90% Wednesday. LA DWP 5s of 2025 at 2.55% versus 2.60% original on 12/8. California 5s of 2026 at 2.51%.

Minnesota 5s of 2028 at 2.41%-2.40% versus 2.47% Wednesday and 2.46% on 12/8. Washington 5s of 2029 at 2.39%. NYC TFA 5s of 2030 at 2.47% versus 2.68% original on 12/8.

California 5s of 2032 at 2.36% versus 2.54% on 12/6 and 2.60% on 12/5. NYC TFA 5s of 2033 at 2.56%-2.51% versus 2.69% Wednesday and 2.76% original on 12/8. Massachusetts 5s of 2034 at 2.44%-2.43%.

San Diego County 5s of 2048 at 3.63%-3.64% versus 3.86% original on 12/6. San Diego USD 5s of 2053 at 3.70%-3.69% versus 3.80% Wednesday and 3.79% Tuesday.

AAA scales

Refinitiv MMD’s scale was bumped 17 basis points: The one-year was at 2.73% (-17) and 2.58% (-17) in two years. The five-year was at 2.33% (-17), the 10-year at 2.36% (-17) and the 30-year at 3.57% (-17) at 3 p.m.

The ICE AAA yield curve was bumped 13 to 16 basis points: 2.76% (-13) in 2024 and 2.59% (-13) in 2025. The five-year was at 2.31% (-15), the 10-year was at 2.37% (-15) and the 30-year was at 3.54% (-13) at 4 p.m.

The S&P Global Market Intelligence municipal curve was bumped 15 to 16 basis points: The one-year was at 2.74% (-16) in 2024 and 2.61% (-16) in 2025. The five-year was at 2.40% (-16), the 10-year was at 2.50% (-15) and the 30-year yield was at 3.52% (-16), according to a 4 p.m. read.

Bloomberg BVAL was bumped 14 to 16 basis points: 2.63% (-15) in 2024 and 2.55% (-15) in 2025. The five-year at 2.28% (-15), the 10-year at 2.36% (-15) and the 30-year at 3.45% (-15) at 4 p.m.

Treasuries rallied.

The two-year UST was yielding 4.381% (-6), the three-year was at 4.083% (-8), the five-year at 3.895% (-9), the 10-year at 3.911% (-12), the 20-year at 4.195% (-14) and the 30-year Treasury was yielding 4.027% (-16) at the close.

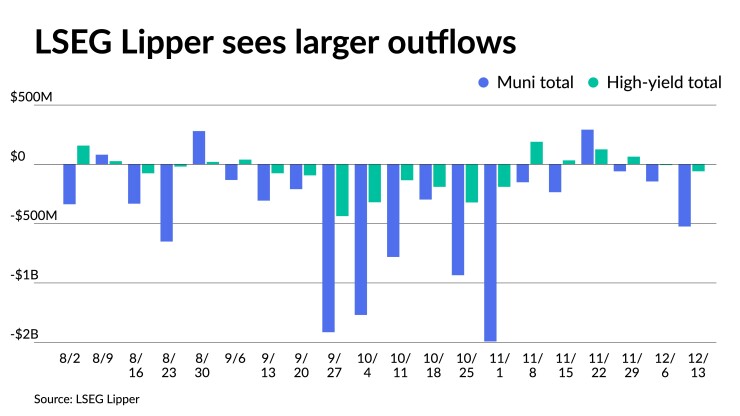

Fund flows

LSEG Lipper reported Thursday that investors pulled $524.3 million from muni mutual funds for the week ending Wednesday after outflows of $144.4 million the week prior.

High-yield saw outflows of $58.4 million after outflows of $58.4 million the week prior.

Strength likely to continue for the asset class

There’s still some broad-based strength across the board in the muni market, said Jeff Timlin, a managing partner at Sage Advisory.

There are around $50 billion in maturities and coupon payments coming due between Dec. 1 and Jan. 15, most of which will probably be reinvested, he said.

“That’s going to be a stabilizer,” he said.

Seasonals and historic returns in December and January tend to be positive, but there are exceptions, according to Timlin.

January 2022 marked a tremendous selloff in the fixed-income markets that contributed to a “pretty significant” down month, but outside of that, “you can see the seasonal effects of December and January in terms of how that affects the supply and demand dynamic in favor of being a seller’s market,” he said.

Other supportive factors include the “proverbial FOMO,” he noted.

Investors see the positive returns and dive in.

There are also market participants making adjustments before yearend numbers, he said.

“There’s a portion of people who are trying to get that final money to work or making adjustments before yearend so that they can go into 2024 with their appropriate asset allocation,” Timlin said.

Munis, he noted, “are probably popping up on a few more people’s radar for various reasons.”

There’s also another dynamic that “could push a significant pool of money into duration products: the tremendous amount of money in money market funds or short-dated liquidity-type funds,” he said.

Short-term rates on those products were 4.5%, and now they’re down to 3% or through it in some instances, he said.

“That’s a huge drop in income, and not only did they lose out on the income instantaneously, but they also missed out on the tremendous return,” Timlin said.

“Then in conjunction with that, there is the differential between what you can get on municipal intermediate products, somewhere with an average life of five years,” he said. “You’re not giving up too much income or yield relative to the money market, but you’re locking it in.”

Market participants may think it’s time to restart this strategy and put money into duration products instead of “playing the short-term game over investing daily,” he said.

However, the worst thing that can happen to investors is if the Fed starts cutting rates, which the market anticipates happening in 2024, according to Timlin.

“If that’s the case, what’s going to be hurt the most is the front end of the curve,” he said. Most investors know the Fed does not stop and start quickly; “It’s going to be a long sustained process.”

That will continue to put pressure on the long end of the curve “in terms of rates going lower,” he said.

Muni CUSIP requests rise

Municipal CUSIP request volume rose in November on a year-over-year basis, following an increase in October, according to CUSIP Global Services.

For muni bonds specifically, there was an increase of 8.5% month-over-month, but a 7.4% decrease year-over-year.

The aggregate total of identifier requests for new municipal securities, including municipal bonds, long-term and short-term notes, and commercial paper, rose 2.7% versus October totals. On a year-over-year basis, overall municipal volumes were down 6%. CUSIP requests are an indicator of future issuance.

FOMC redux

The Federal Open Market Committee could begin cutting rates in April, Arthur Laffer, Jr., president of Laffer Tengler Investments.

The 10-year rates will move back to the 4.5% range “around year-end/beginning of January,” he suggested. “Profit taking from the recent run-up and a full calendar of U.S. debt issuance as far as the eye can see plus continued Fed balance sheet unwinding will keep pressure on rates staying higher in the short run.”

Although “the JOLTs numbers are moving in the right direction if you want indications that wage pressure can ease,” Laffer said, “these numbers are still impressive and indicate labor is still tight.”

Given Fed Chair Jerome Powell’s patience, Jay Woods, chief global strategist at Freedom Capital Markets, expects the first cut will be in May. “The need for a cut at this time would be premature and those thinking we get one by March may be jumping the gun.”

And the projections end the recent debate “about whether investors are getting ahead of themselves,” said Craig Erlam, senior market analyst at OANDA. “The message from the central bank is that is not the case. And in typical fashion, investors have now gone further, pricing in six rate cuts next year starting in March.”

David Page, head of macro research at AXA Investment Managers, said, “We assume that the Fed would have wanted to gently push back on market expectations of rate cuts beginning soon and sharply next year. Yet despite delivering some of the lines necessary, Powell’s broader commentary has served the opposite.”

The markets, especially in the “short-term rates moved to price more cuts,” expecting a March cut, he noted. “November’s contract now suggests rates around 4.00% (more than 5 cuts) having dropped 30bps [since Powell spoke]. 2-year UST yields fell 21bps to 4.46% and 10-year dropped 13bps to 4.03%.”

The market is now convinced rates have peaked, said Brandon Swensen, BlueBay senior portfolio manager of fixed income at RBC Global Asset Management. “This development will be positive for fixed income returns and remains a key reason we are constructive on fixed income looking into next year.”

But despite the dovish shift, there are no guarantees, noted Christian Scherrmann, U.S. economist at DWS Group. “We would like to remind that they are not yet on autopilot to the runway and that the timing of the first rate cuts still depends on the evolution of the income data and, in particular, of inflation.”

Disappointment is possible, he added, “After all, the Fed told us at the last meeting in 2023 that rates are probably high enough, but not how long they need to stay there. The longer in higher for longer will now be the subject of a broader discussion in the coming months.”

Gary Siegel contributed to this story.