The focus shifted fully into the primary market Tuesday as the secondary took a backseat to large new-issues pricing in both negotiated and competitive markets while U.S. Treasuries halted its two-day sell off to see gains on the day. Equities ended mixed.

Munis were little changed Tuesday, as UST yields fell six to nine basis points.

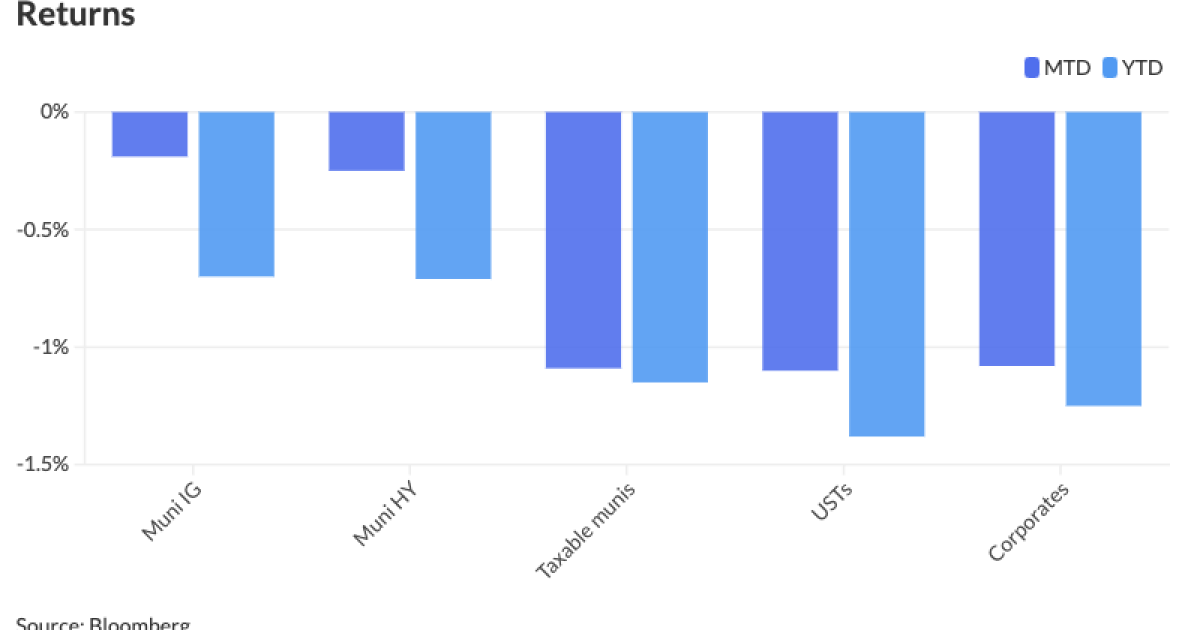

The volatility in USTs is giving municipals a difficult run to start February. The asset class has

“I don’t know what Treasuries are going to do because one day it’s risk-off and the next day it’s a risk on, and that’s creating a whole different environment,” said Jeff Timlin, a managing partner at Sage Advisory.

Ratios rose slightly as a result of the day’s moves. The two-year muni-to-Treasury ratio Tuesday was at 62%, the three-year at 62%, the five-year at 60%, the 10-year at 59% and the 30-year at 83%, according to Refinitiv Municipal Market Data’s 3 p.m. EST read. ICE Data Services had the two-year at 62%, the three-year at 61%, the five-year at 60%, the 10-year at 60% and the 30-year at 82% at 3:30 p.m.

The primary came alive Tuesday and several bellwether credits came to market.

In the negotiated market, Siebert Williams Shank & Co. held a one-day retail order period for $1 billion of tax-exempt future tax-secured subordinate bonds, Fiscal 2024 Series F, Subseries F-1, from the New York City Transitional Finance Authority (Aa1/AAA/AAA/), with 5s of 2/2036 at 2.81%, 5s of 2039 at 3.17%, 5s of 2044 at 3.58%, 5s of 2049 at 3.89% and 4.25s of 2054 at 4.32%, callable 2/1/2034.

RBC Capital Markets priced for the Aldine Independent School District, Texas, (Aaa/AAA//) $343.375 million of PSF-insured unlimited tax school building bonds, Series 2024, with 5s of 2/2025 at 3.13%, 5s of 2029 at 2.63%, 5s of 2034 at 2.68%, 5s of 2039 at 3.16%, 5s of 2044 at 3.53%, 4s of 2049 at 4.20% and 4s of 2054 at 4.26%, callable 2/15/2034.

Jefferies priced for the Houston Higher Education Finance Corp. (Aaa/AAA//) $290.400 million of Rice University Project higher education revenue bonds, Series 2024, with 5s of 5/2034 at 2.64%.

RBC Capital Markets priced for the Wisconsin Housing and Economic Development Authority (Aa2/AA+//) $190 million of non-AMT social home ownership revenue bonds, 2024 Series A, with 3.25s of 9/2026 at par, 3.45s of 3/2029 at par, 3.5s of 9/2029 at par, 3.625s of 3/2034 at 3.71%, 3.8s of 9/2034 at par, 4.05s of 3/2039 at par, 4.375s of 9/2044 at 4.50%, 4.75s of 9/2050 at par and 6s of 9/2054 at 3.86%, callable 3/1/2033.

In the competitive market, Wisconsin (Aa1/AA+//) sold $254.450 million of GOs, Series 2024A, to J.P. Morgan, with 5s of 5/2025 at 3.00%, 5s of 2029 at 2.46%, 5s of 2034 at 2.51%, 5s of 2039 at 3.07% and 5s of 2044 at 3.42%, callable 5/1/2033.

The Osseo Independent School District No. 279, Minnesota, sold $238.350 million of GO school building and facilities maintenance bonds, Series 2024A, to J.P. Morgan, with 5s of 2/2025 at 3.05%, 5s of 2029 at 2.49%, 5s of 2034 at 2.58%, 4s of 2039 at 3.62% and 4s of 2044 at 3.80%, callable 2/1/2032.

The University of Kentucky (Aa2/AA+//) sold $162.955 million of tax-exempt general receipt bonds, 2024 Series B, to Jefferies, with 5s of 4/2030 at 2.55%, 5s of 2034 at 2.58%, 4s of 2039 at 3.65% and 4s of 2044 at par, callable 4/1/2033.

More large new-issues are on the horizon over the next 30 days, including two hefty New York deals.

The Dormitory Authority of the State of New York is set to price $3.5 billion of state personal income tax bonds during the week of March 11.

New York City is set to price $1.3 billion of GOs during the week of Feb. 26.

Despite these deals, Cooper Howard, a fixed-income strategist at Charles Schwab, said it’s possible supply will be slow moving forward after January proved to be an “active” month for new issuance.

Despite the uptick in issuance, it was not enough to prevent “pretty significant” negative net supply in January, Timlin said.

Negative net supply will continue into February, he said. The 30-day net supply sits at negative $12.4 billion, according to Bloomberg data. Bond Buyer 30-day visible supply sits at $8.18 billion.

The slowing of issuance would “bode well” for returns moving forward, Howard said.

Following the late rally during the final few days of January, munis ended the month only down 0.51%, said Jason Wong, vice president of municipals at AmeriVet Securities.

“January is typically a positive month for munis and with the strong end to 2023 that we experienced, we anticipated the month of January to be no different,” he said. “Unfortunately, munis followed suit with Treasuries bringing January into their third losing January in a decade, and the worse return since 2011.”

Munis are currently returning negative 0.19% month-to-date and negative 0.70% year-to-date.

However, if “a rate rally is on the horizon, and historical evidence does seem to support that premise, it will lead to improving total returns that will lead to a feedback loop,” said Vikram Rai, head of municipal market strategy at Wells Fargo.

Secondary trading

Maryland 5s of 2025 at 2.94%. Georgia 4s of 2026 at 2.71% versus 2.73%-2.70% Monday. Washington 5s of 2026 at 2.73% versus 2.78% Monday.

Loudoun County, Virginia, 5s of 2028 at 2.45%. NYC 5s of 2029 at 2.56%-2.55% versus 2.42% Friday and 2.38% Thursday. Boston 5s of 2030 at 2.29%.

California Educational Facilities Authority 5s of 2032 at 2.19%-2.18%. Austin ISD 5s of 2035 at 2.65% versus 2.62%-2.63% Thursday and 2.71% on 1/29. Washington 5s of 2036 at 2.75% versus 2.85% original on 1/24.

Conroe ISD, Texas, 5s of 2049 at 3.77% versus 3.64%-3.50% Monday and 3.57%-3.56% Thursday. Judson ISD, Texas, 4s of 2053 at 4.19% versus 4.12% on 1/31 and 4.19% on 1/30.

AAA scales

Refinitiv MMD’s scale was little changed: The one-year was at 2.99% (-2) and 2.73% (unch) in two years. The five-year was at 2.41% (unch), the 10-year at 2.43% (unch) and the 30-year at 3.57% (unch) at 3 p.m.

The ICE AAA yield curve was little changed: 2.99% (+2) in 2025 and 2.77% (+2) in 2026. The five-year was at 2.47% (unch), the 10-year was at 2.46% (unch) and the 30-year was at 3.55% (unch) at 3:30 p.m.

The S&P Global Market Intelligence municipal curve was unchanged: The one-year was at 3.00% in 2025 and 2.78% in 2026. The five-year was at 2.46%, the 10-year was at 2.46% and the 30-year yield was at 3.55%, according to a 3 p.m. read.

Bloomberg BVAL was unchanged: 2.92% in 2025 and 2.77% in 2026. The five-year at 2.43%, the 10-year at 2.50% and the 30-year at 3.60% at 3:30 p.m.

Treasuries were firmer.

The two-year UST was yielding 4.401% (-8), the three-year was at 4.189% (-8), the five-year at 4.032% (-9), the 10-year at 4.084% (-8), the 20-year at 4.387% (-7) and the 30-year Treasury was yielding 4.286% (-6) at 3:45 p.m.

Primary on Monday

Morgan Stanley priced for the Southeast Alabama Gas Supply District (A1///) $820.115 million of Project No. 2 gas supply revenue refunding bonds, Series 2024B, with 5s of 11/2024 at 4.45%, 5s of 5/2029 at 4.11%, 5s of 11/2029 at 4.11%, 5s of 5/2032 at 4.27% and 5s of 6/2049 with a mandatory tender date of 5/1/2032 at 4.32%, callable 2/1/2032.

Primary to come:

Massachusetts (Aa1/AA+/AA+/) is set to price Wednesday $540 million of GO refunding bonds, 2024 Series B. Jefferies.

The Illinois Housing Development Authority (Aaa///) is set to price Thursday $495 million of social revenue bonds, consisting of $145 million of non-AMT bonds, 2024 Series A, and $350 million of taxable, 2024 Series B. RBC Capital Markets.

The East Bay Municipal Utility District, California, (Aaa/AAA//) is set to price Wednesday $432.355 million of water sewer revenue bonds, consisting of $248.250 million of green bonds, Series 2024A, and $184.105 million of refunding bonds, Series 2024B. J.P. Morgan.

The University of Washington (Aaa/AA+//) is set to price Thursday $304.515 million of general revenue bonds, consisting of $222.190 million of new-issue bonds, Series 2024A, serials 2025-2044; and $82.325 million of refunding bonds, Series 2024B, serials 2024-2041. BofA Securities.

The Clifton Higher Education Finance Corp., Texas, (Aaa///) is set to price Thursday $293.710 million of PSF-insured International Leadership of Texas education revenue and refunding bonds, consisting of $209.810 million of Series 2024A and $83.900 million of Series 2024B. RBC Capital Markets.

The Oklahoma County Finance Authority (A1/A+//) is set to price Thursday $240.825 million of Midwest City-Del City Public Schools Project educational facilities lease revenue bonds, Series 2024. D.A. Davidson.

The San Diego Community College District (Aa1/AAA//) is set to price Wednesday $100 million of 2024 dedicated unlimited ad valorem property tax GO refunding bonds. RBC Capital Markets.

Competitive

Wisconsin is set to sell $150 million of green Environmental Improvement Fund revenue bonds, Series 2024A, at 10:45 a.m. Wednesday.

The New York City Transitional Finance Authority is set to sell $250 million of taxable future tax-secured subordinate bonds, Fiscal 2024 Series F, Subseries F-2, at 11:15 a.m. Wednesday.

The Washington Suburban Sanitary District, Maryland, is set to sell $329.240 million of consolidated public improvement bonds of 2024 at 10:15 a.m. Thursday.