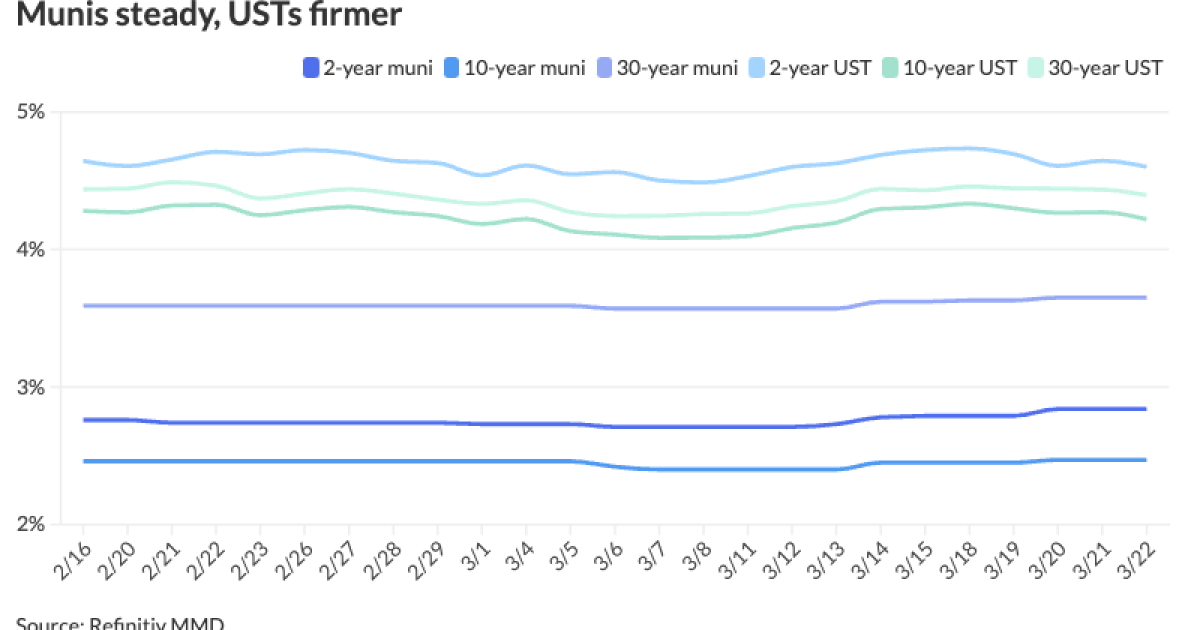

Municipals were steady to end the week ahead of a surge in supply, helped by three billion-plus deals. U.S. Treasuries were firmer and equities were mixed.

While USTs yields fell up to five basis points late in the session Friday, they sold off for most of this week, with various market participants seeing “even more downside for long rates ahead,” said Barclays PLC in a weekly report.

Municipals went their own way, but did see pressure this week with the front-end cheapening, “and this actually happened when supply was relatively light,” noted Barclays strategists Mikhail Foux, Clare Pickering and Mayur Patel.

Munis appeared to be “taking the first dose of tax time weakness, with 0-3yr AAA yields rising significantly on Wednesday as ratios to Treasuries rose more than 3ppt from recent lows,” said BofA strategists.

Long maturity yields also “rose modestly,” but muni-UST ratios did not move much, they noted.

The two-year muni-to-Treasury ratio Friday was at 62%, the three-year at 61%, the five-year at 59%, the 10-year at 59% and the 30-year at 83%, according to Refinitiv Municipal Market Data’s 3 p.m. EST read. ICE Data Services had the two-year at 62%, the three-year at 61%, the five-year at 59%, the 10-year at 59% and the 30-year at 81% at 3:30 p.m.

Issuance will be heavy next week, with the new-issue calendar estimated at $9.190 billion, with $8.471 billion of negotiated deals and $718.5 million of competitive deals on tap.

The negotiated calendar is led by $2.7 billion of GOs from California, followed by

The Santa Clara Unified School District, California, leads the competitive calendar with $128.3 million of GO refunding bonds.

High-yield gets another does of unrated project finance bonds, this week from the Public Finance Authority’s $243.185 million of Miami Worldcenter Project tax increment revenue bonds. This comes following the healthy appetite for unrated paper demonstrated Tuesday with Keybank’s pricing of the

The rise in issuance may lead to more muni underperformance, but Barclays strategists do not think muni-UST ratios will move “meaningfully higher, as buyers would likely emerge.”

However, BofA strategists argue if UST yields 10 years and out rise as expected, muni-UST ratios should “rise some from record low levels as well, but should still prove quite resilient.”

BofA strategists said “both the muni AAA curve and muni ratio curve should have some bear flattening while Treasuries steepen for the next several week.”

Elsewhere, in the taxable space, Build America Bonds and extraordinary redemption provisions unsurprisingly remain the “topic du jour,” said Barclays strategists.

The most recent developments include

For the former, legal actions could follow if the issuer does not abide by the requests.

“Other issuers that either exercised their ERP calls already or are intending to exercise them in the near future could potentially receive similar letters,” Barclays strategists said.

While several other issuers have decided to call their BABs through an ERP, they said “this development will likely give a bit of a pause to issuers that were intending to exercise their calls.”

BAB spreads have “continued underperforming,” but in the near term recent developments could support them, they said.

Separately, Barclays strategists noted, that the market might see “tax-exempts issued recently to take out BABs via ERPs start trading at a bit of discount due to this legal uncertainty.”

AAA scales

Refinitiv MMD’s scale was unchanged: The one-year was at 3.07% and 2.84% in two years. The five-year was at 2.47%, the 10-year at 2.47% and the 30-year at 3.65% at 3 p.m.

The ICE AAA yield curve was bumped up to two basis points outside of one year: 3.14% (+1) in 2025 and 2.89% (unch) in 2026. The five-year was at 2.52% (-1), the 10-year was at 2.49% (-1) and the 30-year was at 3.58% (-1) at 3:30 p.m.

The S&P Global Market Intelligence municipal curve was unchanged: The one-year was at 3.08% in 2025 and 2.86% in 2026. The five-year was at 2.50%, the 10-year was at 2.49% and the 30-year yield was at 3.62%, according to a 3 p.m. read.

Bloomberg BVAL was unchanged: 3.06% in 2025 and 2.87% in 2026. The five-year at 2.45%, the 10-year at 2.46% and the 30-year at 3.63% at 3:30 p.m.

Treasuries were firmer.

The two-year UST was yielding 4.601% (-4), the three-year was at 4.370% (-5), the five-year at 4.202% (-6), the 10-year at 4.219% (-5), the 20-year at 4.483% (-5) and the 30-year at 4.394% (-4) at 3:30 p.m.

Primary to come

California is set to price Tuesday $2.671 billion of various purpose GOs, consisting of $1.312 million of new-issue bonds and $1.359 billion of refunding bonds. J.P. Morgan.

New York City (Aa2/AA/AA/AA+/) is set to price Tuesday $1.452 billion of GOs, consisting of $1.100 billion of Fiscal 2024 Series D, serials 2026-2049, term 2054; $163.815 million of Fiscal 2024 Series E, serials 2025-2035; $15.230 million of Fiscal 2024 Series F, serials 2024-2035; $108.365 million of Fiscal 2024 Series I-4, serials 2028-2036; and $65.020 million of Fiscal 2024 Series I-5, serials 2028-2036. Jefferies.

Washington (Aaa/AA+/AA+/) is set to price Tuesday $1.083 billion of motor vehicle fuel tax and vehicle relate fees GO refunding bonds, Series R-2024C, serials 2024-2040. Wells Fargo.

The Austin Independent School District (Aaa///AAA/) is set to price Monday $720.930 million of PSF-insured unlimited tax school building bonds, Series 2024, serials 2026-2044, term 2049. Cabrera Capital Markets.

The Northern California Energy Authority is set to price $675 million of commodity supply revenue refunding bonds, Series 2024. Goldman Sachs.

The Michigan Finance Authority (A3///) is set to price Tuesday $248.250 million of green Henry Ford Health Detroit South Campus Central Utility Plant Project Act 38 facilities senior revenue bonds, Series 2024. J.P. Morgan.

The Public Finance Authority is set to price Tuesday $243.185 million of Miami Worldcenter Project tax increment revenue bonds, consisting of $192.540 million of senior bonds, Series 2024A, and $50.645 million of subordinate bonds, Series 2024B. D.A. Davidson.

The South Dakota Housing Development Authority (Aaa/AAA//) is set to price Wednesday $148 million of homeownership mortgage bonds, consisting of $99 million of non-AMT bonds, 2024 Series A, terms 2044, 2049, 2055, and $49 million of taxables, 2024 Series B, serials 2025-2036, terms 2039, 2040. BofA Securities.

The Hospital Authority of Valdosta and Lowndes County, Georgia, (Aa2/AA-//) and is set to price Tuesday $129.500 million of South Georgia Medical Center Project revenue anticipation certificates, Series 2024, serials 2025-2044, terms 2049, 2054. Raymond James.

The Rockdale County Public Facilities Authority (Aa2///) is set to price Monday $123.650 million, consisting of $110 million of revenue bonds, Series 2024, and $13.650 million of GO sales tax bonds, Series 2024. J.P. Morgan.

The Wisconsin Health And Educational Facilities Authority (//BBB-/) is set to price Tuesday $108.860 million of Three Pillars Senior Living Communities revenue bonds, consisting of $63.215 million of Series A, $8.055 million of Series B-1 and $37.590 million of Series B-2.. KeyBanc Capital Markets.

Competitive

Oklahoma City, Oklahoma, is set to sell $110.220 million of GOs, Series 2024, at 9:30 a.m. eastern Tuesday, and $10.280 million of taxable GOs, Series 2024, at 9:45 a.m. Tuesday.

The Santa Clara Unified School District, California, (Aaa/AAA//) is set to sell $148.260 of 2024 GO refunding bonds at 11:05 a.m. Wednesday.