Municipals were little changed Thursday with the last of the largest deals pricing while municipal bond mutual funds reported a return to outflows. U.S. Treasury yields fell and equities were up near the close.

The two-year muni-to-Treasury ratio Thursday was at 66%, the three-year at 66%, the five-year at 67%, the 10-year at 66% and the 30-year at 84%, according to Refinitiv Municipal Market Data’s 3 p.m. EST read. ICE Data Services had the two-year at 65%, the three-year at 67%, the five-year at 67%, the 10-year at 67% and the 30-year at 84% at 3:30 p.m.

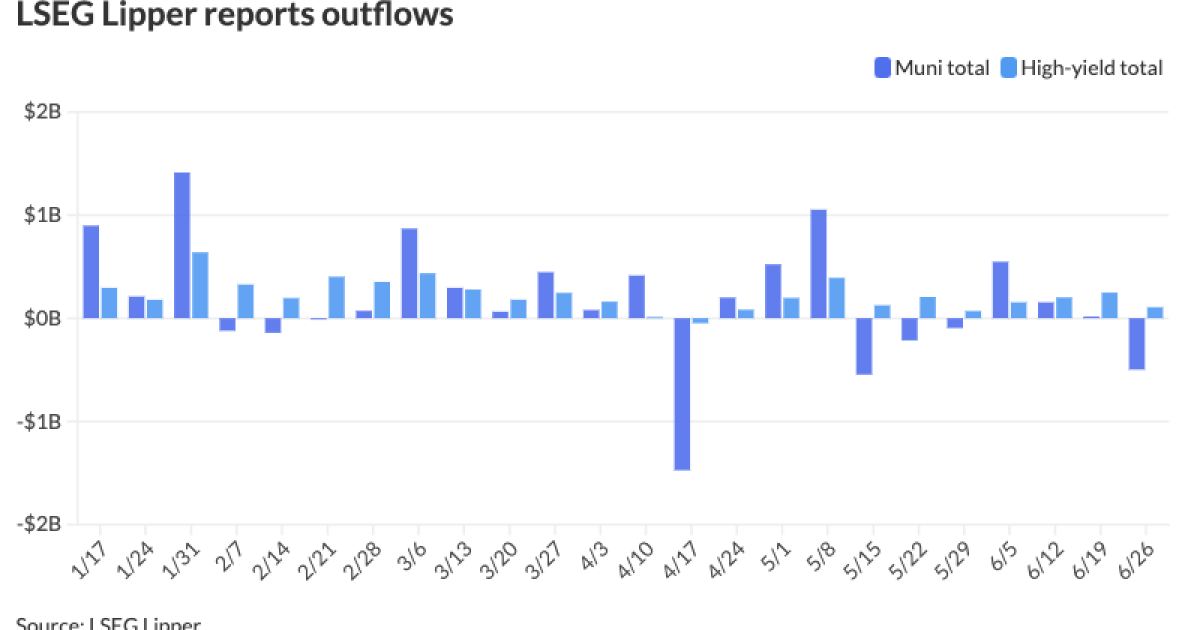

Municipal bond mutual funds saw outflows as investors pulled $498 million from funds after $16 million of inflows the week prior, according to LSEG Lipper. Outflows this week were led by long-term funds.

High-yield continued to show strength, with inflows of $107 million after $248.9 million of inflows the previous week.

Investment demand has slowed, which is unsurprising “given where we are in the calendar,” noted Pat Luby, head of municipal strategy at CreditSights.

Between the Federal Open Market Committee meeting two weeks ago and the holiday-shortened week last week, that has “distorted everything,” making it hard to get a “clear read” on demand, Luby said.

Last week’s

This week features a surging new-issue calendar of over $12 billion to close out June, helping to secure six months of issuance gains.

In the primary market Thursday, Morgan Stanley priced and repriced for institutions $1.086 billion of senior sales tax bonds from the Massachusetts Bay Transportation Authority (/AA+/AAA/AAA/), with two to 13 basis point cuts from Wednesday’s retail pricing. The first tranche, $987.635 million of 2024 Series A, saw 5s of 7/2025 at 3.25% (+11), 5s of 2029 at 3.07% (+7), 5s of 2034 at 3.12% (+12), 5s of 2039 at 3.39% (+11), 4s of 2044 at 4.07% (+2), 5s of 2044 at 3.74% (+10), 5s of 2048 at 3.95% (+13), and 5s of 2052 at 3.98% (+6), callable 7/1/2034.

The second tranche, $97.705 million of sustainability bonds, 2024 Series B, saw 5s of 7/2054 at 4.00% (+6), callable 7/1/2034.

Jefferies priced for the State Building Authority of Michigan (Aa2//AA/) $130.665 million of Facilities Program Series II revenue refunding bonds, with 5s of 10/2024 at 3.40%, 5s of 4/2029 at 3.02%, 5s of 10/2029 at 3.02%, 5s of 4/2034 at 3.08%, 5s of 10/2034 at 3.08%, 5s of 4/2036 at 3.18%, 5.25s of 10/2054 at 4.11% and 5.25s of 4/2059 at 4.19%, callable 10/15/2034.

Siebert Williams Shank priced for the Lewisville Independent School District, Texas, (/AAA/AAA/) $112.265 million of PSF-insured unlimited tax school building and refunding bonds, with 5s of 8/2025 at 3.33%, 5s of 2029 at 3.14%, 5s of 2034 at 3.22%, 5s of 2039 at 3.46% and 4s of 2044 at 4.13%, callable 8/15/2033.

RBC Capital Markets priced for the Kings Local School District, Ohio, (/AA//) $100 million of school improvement unlimited tax GOs, Series 2024, with 5s of 12/2025 at 3.31%, 5s of 2029 at 3.07%, 5s of 2034 at 3.12%, 5s of 2039 at 3.40%, 5s of 2044 at 3.84%, 5/25s of 2049 at 4.02% and 4.14s of 2054 at 4.14%, callable 6/1/2032.

In the competitive space, Augusta, Georgia, sold $126.395 million of water and sewerage revenue refunding and improvement bonds, Series 2024, to Mesirow Financial, with 5s of 10/2024 at 3.30%, 5s of 2029 at 3.05%, 5s of 2034 at 3.05%, 5s of 2039 at 3.33%, 4s of 2044 at 4.12%, 4s of 2049 at 4.12%, and 5s of 2054 at 4.25%, callable 10/1/2033.

Preliminary issuance for June is at $41.283 billion, up 4% from 2023, according to LSEG data Thursday.

Next week is another holiday-shortened week, with issuance expected to be light.

Following the Fourth of July holiday, Luby said he believes the pace of new-money borrowings will slow, but there may be a “continued appetite” for refundings.

This trend can already be seen in June, with preliminary figures showing new-money down 1.2%, while refundings rise 9.7%, according to LSEG.

The market will get “some relief” next week due to July reinvestment capital, said J.P. Morgan strategists, led by Peter DeGroot.

“As we proceed into summer with lighter holiday supply weeks sandwiched between heavy volume weeks, the flow of reinvestment capital takes on added week-to-week significance,” they said.

The highest tax-exempt coupon/redemption reinvestment of the summer will happen during the first half of July, with July 1 seeing payments of $31 billion, above Aug. 1’s payments of $24 billion, J.P. Morgan strategists said.

Conversely, July 15 will see the lightest payments of the summer at $4 billion and a third of the mid-August coupon/redemption payment of $12 billion, they noted.

These figures exclude the $7 billion in refunding capital expected over the next two months, making up the balance of reinvestment capital in July and August, they said.

AAA scales

Refinitiv MMD’s scale was unchanged: The one-year was at 3.15% and 3.11% in two years. The five-year was at 2.89%, the 10-year at 2.84% and the 30-year at 3.72% at 3 p.m.

The ICE AAA yield curve saw cuts: 3.19% (+5) in 2025 and 3.12% (+3) in 2026. The five-year was at 2.92% (flat), the 10-year was at 2.89% (+2) and the 30-year was at 3.72% (flat) at 3:30 p.m.

The S&P Global Market Intelligence municipal curve was unchanged: The one-year was at 3.16% in 2025 and 3.10% in 2026. The five-year was at 2.88%, the 10-year was at 2.87% and the 30-year yield was at 3.70% at 3 p.m.

Bloomberg BVAL was unchanged: 3.17% in 2025 and 3.12% in 2026. The five-year at 2.93%, the 10-year at 2.84% and the 30-year at 3.73% at 3:30 p.m.

Treasuries were firmer.

The two-year UST was yielding 4.717% (-3), the three-year was at 4.498% (-3), the five-year at 4.302% (-3), the 10-year at 4.291% (-3), the 20-year at 4.537% (-2) and the 30-year at 4.430% (-2) at 3:45 p.m.